Entrepreneurial Mothers: Balancing Business and Family with Expertise

The motherhood penalty is the wedge

Most of what's written about the so-called mompreneur question opens by celebrating the balance. This one will not. Let's start with the number nobody on the first page of Google has bothered to put in front of you. In 2024, full-time working mothers in the United States earned a median of $56,680. Full-time working fathers earned $76,388. That is a 35% pay gap, wider than 2023 (31%) and wider than 2022 (32%), and over a thirty-year career it works out to roughly $591,000 in lost wages per mother (Bankrate analysis of Census Bureau CPS). This is the motherhood penalty, and it is the most useful frame for thinking about why a mother starts her own business.

The standard essay on this topic opens by celebrating the balance. The standard essay is wrong. Most mothers who launch a business are not chasing a lifestyle brand. They are responding to a documented, structural earnings shortfall — the kind that does not narrow with grit or great childcare, the kind that compounds for thirty years. A mom-owned business is, among other things, a hedge. It can absorb a school-pickup schedule that an employer cannot, and it can recapture some of the income an employer is structurally paying less of in the first place. That is not an aspirational frame. It is the frame.

If you only read one statistic from this article, make it the $591,000. The rest of the piece is about what to do about it.

Who actually runs mom-owned businesses

There are about 4.2 million U.S. small businesses owned by mothers. They generate roughly $3.9 trillion in annual revenue and employ around ten million people — about one in three women-owned firms is mom-owned (Mompowerment, citing SBA Office of Advocacy and Wells Fargo's Impact of Women-Owned Businesses 2024). That is a real population. It is not a niche.

The demographic profile pushes back on the lifestyle-brand stereotype. A 99designs survey of 1,290 business-owner parents found that 57% are 40 or older, 95% have a partner who brings in income, and roughly 71% are also their children's primary caregiver (reported by Entrepreneur.com). Translate that: the typical mom business owner is in her forties, doing the bulk of unpaid domestic labour, and running a venture that sits next to — not instead of — a household partner's salary. The household relies on her income; it does not always rely on her income to cover rent.

That detail matters because it sets the financial decision frame. If you are the household's second income, the question "should I formalize my side hustle?" is really "is the marginal tax saving plus liability protection worth the formation cost and the quarterly bookkeeping?" If you are the household's first income (single mothers, separated parents, partners on parental leave), the question is much closer to "can I clear the fixed cost of childcare every month, every month, without flinching?" Same business, very different math.

What "boundaries" actually means: the cost of an hour

Most articles in this space tell mothers to set clear boundaries between work and family. Then they move on. Let's not move on.

A boundary is just a budget for your time. The useful version is to pick the hours your business runs and to price every other hour at your own hourly rate — not your billable rate, your own. If you can earn $80 an hour billable but you accept work between 5pm and 9pm on a weeknight, you are taking a $320 evening at the cost of childcare you do not have, plus the hidden cost of doing the bedtime shift at sub-optimal capacity afterwards. That is not a $320 evening. It is, generously, a $180 one. Often less.

The mechanic that follows is unglamorous. Set the hours. Refuse the spillover. Charge premium rates inside the hours so the spillover never needs to happen. The mothers who survive this are not the ones with stronger willpower; they are the ones whose pricing structure makes the boundary financially possible. If your rates do not let you turn down a 6pm meeting, the problem is not your boundaries — it's the rate card.

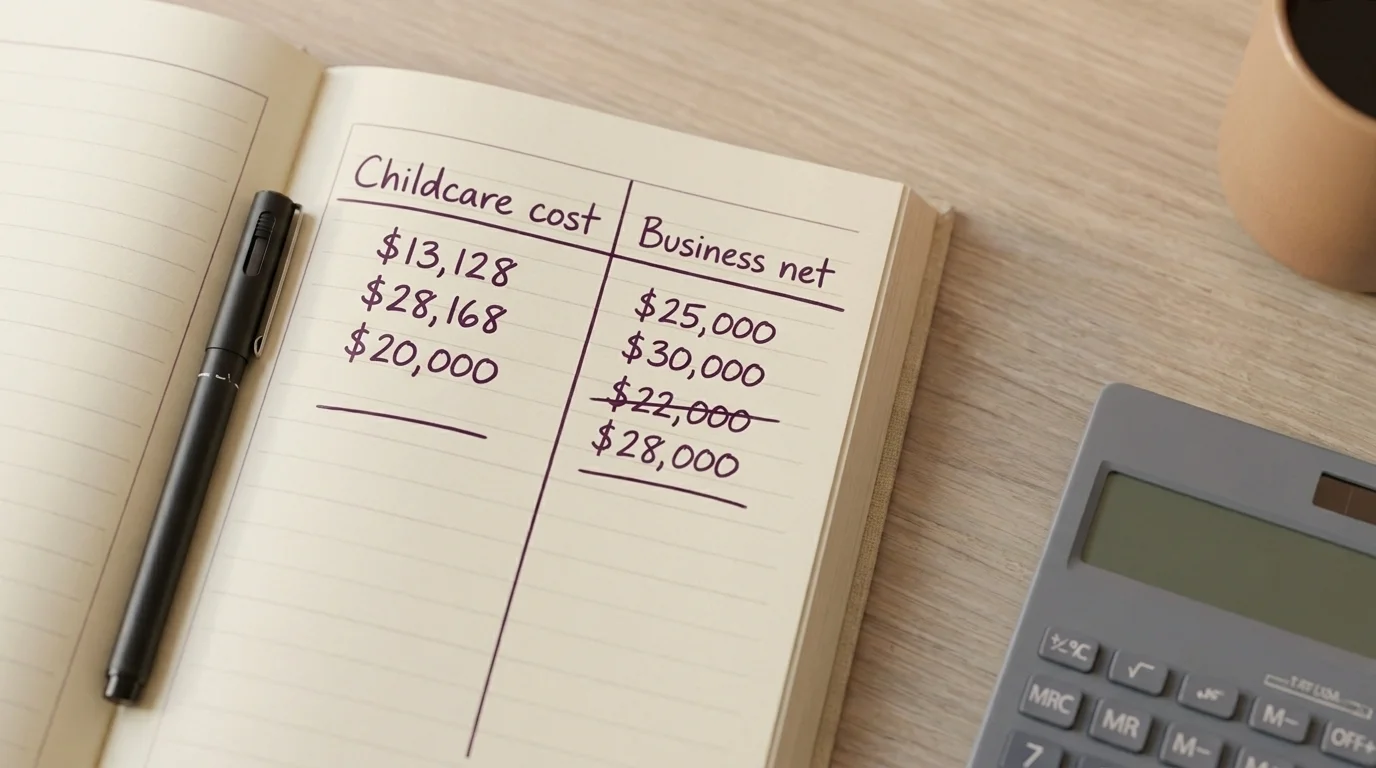

Childcare break-even: when paid care pays for itself

Childcare in the US is not a line item. It is a regime. Center-based infant care now averages $13,128 per child per year. Two children — say an infant plus a toddler — averages $28,168. In nine states the average childcare bill exceeds $20,000 per child, and the federal Department of Health and Human Services affordability threshold (7% of family income) is met in zero states for families at the local median income (CNBC analysis).

Treat that the way you would treat a mortgage — a fixed obligation your variable income has to clear every single month, indifferent to whether you booked a good client this week.

The useful question is the break-even one. At roughly $13,000 per child per year for paid childcare, your business needs to net (after self-employment tax and any income tax) about $13,000 per child before paid care pays for itself in pure dollar terms. That is roughly $25,000–$30,000 of freelance revenue per child, depending on your tax bracket and whether you qualify for the QBI deduction (we will get to that). Below that revenue threshold, you are paying out of pocket for the privilege of working — which can still be the right call, because experience, network, and the optionality of a viable business have value beyond the current year's P&L. Above that threshold, the math turns. Knowing where you sit on that line is more useful than any motivational essay about pursuing your passion.

Tax mechanics worth pricing (US)

This is the section other essays skip. It should not be the section other essays skip.

Three US tax provisions move real money for self-employed mothers, and any honest piece on running a business as a parent has to name them. None of this is tax advice — confirm everything with a CPA who knows your state and your filing status.

Section 199A, the QBI deduction. If you operate a qualified trade or business as a sole proprietor, single-member LLC, partnership, or S-corp, you can generally deduct up to 20% of your qualified business income from your taxable income. For tax year 2025, the deduction is fully available below taxable income thresholds of $247,300 (single filers) or $494,600 (joint filers), and phases out above (summary of §199A 2025 limits). The One Big Beautiful Bill Act made §199A permanent and, starting in tax year 2026, added a $400 minimum QBI deduction for any active qualified business with at least $1,000 in QBI, plus higher phase-in ranges. In plain English: under the new rules, almost any formalized business with real income gets at least a $400 federal tax break by default. The previous status (deduction expiring after 2025) had created a real planning problem for newly formalized one-person businesses; the OBBBA permanence resolves it. That is a non-trivial reason to bother forming the entity.

Self-employment tax and the S-corp inflection. Once your net business income comfortably clears about $80,000–$100,000, electing S-corp status can save meaningful self-employment tax by splitting your take-home into a reasonable salary (subject to FICA) and a distribution (not subject to FICA). Below that band the additional bookkeeping and payroll cost usually outweighs the saving. Above it, it usually doesn't. The threshold depends on your state, your payroll provider, and what counts as a "reasonable salary" in your industry — this is the textbook example of a question to ask an accountant rather than the internet.

Retirement: SEP IRA and Solo 401(k). A Solo 401(k) lets a self-employed parent contribute as both employee (up to the standard 401(k) limit) and employer (up to 25% of net self-employment earnings), which makes it the higher-ceiling vehicle in most years. A SEP IRA is simpler to set up but caps at the employer-side contribution only. For a mom-owned business clearing $60,000 net, the Solo 401(k) typically allows substantially more sheltered savings than the SEP IRA — exactly the point at which the motherhood-penalty wedge starts to close.

The discipline here is to formalize the business at the revenue level where the tax structure actually changes the answer, and not before. Forming an LLC on $4,000 of side income is paperwork; forming it on $40,000 is a planning decision.

Health insurance after you go self-employed

This is the single largest non-business cost shock that lands on a mother leaving an employer plan, and it is about to get worse in the US.

The enhanced Affordable Care Act premium tax credits are scheduled to expire at the end of 2025. If Congress does not extend them, the Center on Budget and Policy Priorities estimates that out-of-pocket marketplace premiums will rise by 75% or more on average for the families that buy coverage there — and roughly one in four marketplace enrollees is a small-business owner or self-employed worker. That is about five million people, a lot of them parents (CBPP analysis).

For a mother weighing the leap to self-employment in 2026, the realistic options are:

- Stay on a partner's employer plan if you have one. This is by far the cheapest option and is the reason the 95% partnered-income statistic above matters financially.

- Buy on the ACA marketplace with whatever subsidy structure exists at the time you enrol. Run the numbers at healthcare.gov for your income, your state, and your household size — premium variance is enormous.

- Use a Qualified Small Employer HRA (QSEHRA) or Individual Coverage HRA (ICHRA) if you employ anyone, including yourself through an S-corp. These let the business reimburse health premiums on a pre-tax basis. They are the right answer surprisingly often and are routinely missed.

- COBRA from a prior employer, for the bridge months only. It is expensive and time-limited.

Whatever the answer is, price it before you give notice. The number is rarely what people expect.

Named grants and where the money actually is

A Shopify survey of 1,532 US parents found that 55% of women cite funding as a top barrier to starting a business, compared with 41% of men, and 45% cite "not knowing where to start" compared with 29% of men (Shopify research). The funding gap is real. The fact that this article is one of very few in the cluster to name a single actual grant program is also real.

Three programs are worth knowing by name:

- Hello Alice. Runs rolling grants of $10,000 and up, plus periodic cohort grants — one recent cohort awarded $20,000 each to 100 recipients and paired the money with a 12-week Boost Camp accelerator (Hello Alice grants). Eligibility varies by program but typically requires US residency and an established (not pre-launch) business.

- IFundWomen. Runs a universal application database that matches founders to partner grants from Visa, Neutrogena, American Express, and others (IFundWomen grants). The single application is the leverage — you submit once and IFundWomen matches you against open opportunities as they come up.

- Kitty Fund Mompreneur Business Grant (Founders First). A smaller, targeted grant of $1,000 specifically for mother-founders, paired with Founders First's accelerator programming. Cross-referenced in NerdWallet's grant inventory.

Three caveats. First, none of these will fund a business from a standing start — most expect some revenue, some traction, or a clear plan. Second, the grant landscape is volatile; check current eligibility before you spend a Saturday on the application. Third, $1,000 grants are not life-changing money, but the network access that comes with them often is.

Flexibility, the version that actually works

"Be flexible" is what other essays say. The mechanic that delivers it is this: build your client contract and your billing structure to survive a sick kid.

In practice that means flat-fee or milestone-based pricing where possible, not hourly billing — because hourly billing punishes you for the eighty minutes you lost when the school called at 11am. It means a stated turnaround window of three to five business days on most deliverables, not 24 hours — because the longer window absorbs the bad day without a missed deadline. It means a roster of one or two collaborators you can hand a piece of work to during a fever week, and a return-the-favour arrangement that makes the hand-off normal rather than a crisis. The mothers I know who have run businesses for ten years and counting are the ones who put these mechanics in place in year one and stopped apologizing for them in year two.

The version of flexibility that does not work is the one where you simply work later. That is not flexibility. That is the unpaid second shift wearing a costume.

What this means for you

None of this is universal. A mother in a US state with $20,000 infant childcare and no nearby family is solving a different math problem than one in a province with $10-a-day daycare and a parent-in-law next door. A solo founder is solving a different problem than one of a two-income household. The 95th-percentile mother-founder with an MBA, a network, and seed funding is solving a different problem than the freelancer building a $40,000 design practice while her kids are in elementary school.

The point of pricing the tradeoffs is not to find the universal answer. The point is to know which trade you are actually making. The motherhood penalty is the wedge — $591,000 over a career is the wedge. Whether the right response is a formal business, a side income, a renegotiated employment arrangement, or a deliberate pause is a question the spreadsheet has to answer in your jurisdiction, with your numbers, in your household. The honest version of this article is: do the math, name the assumptions, ask the accountant, and stop calling the resulting business a lifestyle choice. It is a financial response to a documented structural problem, and it deserves the dignity of the spreadsheet.

Frequently Asked Questions

A mompreneur is a mother who owns and operates a business — typically while raising children. The term covers full-time founders, side-hustle moms, and stay-at-home parents running home-based ventures. As of 2024, roughly 4.2 million U.S. small businesses are mom-owned, generating about $3.9 trillion in annual revenue (Wells Fargo / SBA via Mompowerment).

Three realistic paths. First, named grants — Hello Alice runs rolling $10,000+ awards plus cohort grants, IFundWomen runs a universal application database that matches founders to partner grants from Visa, Neutrogena, and American Express, and the Kitty Fund Mompreneur Business Grant from Founders First awards $1,000 specifically to mother-founders. Second, service-based businesses with near-zero startup cost: consulting, freelance writing, virtual assistance, bookkeeping. Third, SBA microloans up to $50,000 through the SBA Women's Business Centers network. None will fund you from a standing start — most expect some traction first.

It depends on revenue. Below roughly $40,000/year a sole proprietorship is usually adequate. Between $40,000 and $150,000 a single-member LLC adds liability protection without much tax complexity. Above $150,000 an S-corp election can reduce self-employment tax meaningfully. The 20% QBI deduction under §199A — now permanent under the One Big Beautiful Bill Act — applies to all three structures up to 2025 taxable-income thresholds of $247,300 (single) or $494,600 (joint). Starting in tax year 2026 there is also a $400 minimum QBI deduction for any active qualified business with at least $1,000 in QBI. Confirm with a CPA who knows your state.

The aggregate is $3.9 trillion in annual revenue across about 4.2 million U.S. mom-owned businesses (Wells Fargo / SBA), but that average hides huge variance. A 99designs survey of 1,290+ mom business owners found 95% have a partner who brings in income, which suggests most mom-owned businesses operate as a household second income rather than sole support. The Census-measured motherhood wage penalty was 35% in 2024 — full-time working mothers earned a median of $56,680 vs. fathers' $76,388 (Bankrate) — which is one of the structural reasons mothers launch businesses in the first place.